India’s Growing Maritime Role

As the world’s most populous country and fifth largest economy, India holds a growing role on the global stage. Within parts of the maritime ecosystem, development has been mixed, lagging potential. But as a key hub for operations and crewing, and now the largest seaborne importer after China, ambitions to further develop fleet, ports & shipbuilding have renewed government support.

Shipping Heritage

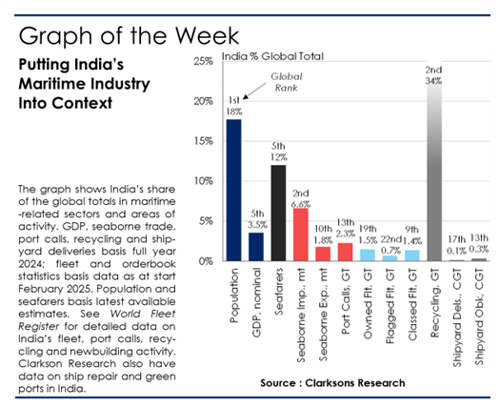

With a population of 1.5 billion, India is the world’s fastest growing major economy (2025f: +7%), and on track to become the third largest globally by 2030. Against this backdrop, India’s role in maritime is evolving, with the government increasing strategic focus on the sector. India is already the fifth largest source of seafarers (~12% of world total, government target ~20%). And India has for many decades been a prominent recycling destination, with facilities handling a third of tonnage recycled 2004-24. In 2024, India ranked second for volumes (~30% share) but Indian recyclers also seem to be leading Bangladesh and Pakistan in preparing facilities for compliance with the HK Convention green treaty (in force from June 2025).

Demand Driver

Across global seaborne trade, India is an increasingly key driver. Over the last decade, Indian seaborne imports grew by a CAGR of 2.9% (global 1.7%, China 4.1%) to reach ~830mt in 2024, 7% of the global total and second only to China (3.2bt, 25%). India is now the second largest importer of a range of key cargoes, including coal (19% of global total), crude oil (12%, including a shift to longer haul Russian crude since 2022) and LPG (16%), and across all cargoes has driven ~15% of growth in global trade in the last decade (again behind only China that has contributed 55% of growth). We project the balance of this growth share will lean towards India in the next decade, with India reaching >1.2bt of imports by 2035 (this would still be a third of China however). Indian exports have shown more muted growth, totalling ~225mt in 2024, 2% of the global total (India: 10th largest exporter), up only slightly vs 2010 (218mt), with oil products exports steady, and more minor bulk and container exports offsetting lower iron ore. Meanwhile, India’s >80 ports handled >70,000 vessel calls last year (largest tonnage handler, Mundra, is only the 50th largest globally with 224.5m GT of port calls in 2024, policy targets three ‘mega’ ports by 2030).

Maritime Goals

The Indian government has a range of policies aiming to strengthen the maritime sector, including across ports, shipbuilding and recycling. Today, India is the 19th largest ship owning cluster (an underweighted ~1.5% of world fleet, headed by SCI, Great Eastern, Chellaram and Seven Islands) and 22nd largest flag state (0.7%), but aims to have a top 5 fleet of 100m GT by 2047. Shipbuilding (and ship repair) has a long history in India (although with a sometimes mixed track record), and policy is targeting a top 10 builder by 2030 and top 5 by 2047 (2024: 13th largest orderbook by CGT, 0.3% share, Cochin leading). Shipbuilding is incredibly competitive (China 58% of orderbook), but there may be good potential initially in smaller ships, supported by fleet renewal and green designs. Policy is also targeting improved efficiency, renewable energy at ports and cruise markets. So lots of growth opportunity but also plenty of challenges ahead if India is to unlock its wider maritime potential.

Clarksons Research have established a local presence in India, including expert teams focused on our marine equipment, green technology and port infrastructure data. Our affiliate, Clarksons Shipbroking, also has a longstanding local presence with a highly experienced team including tanker and dry cargo chartering.

The author of this feature article is Stephen Gordon. Any views or opinions presented are solely those of the author and do not necessarily represent those of the Clarksons group.